Global markets got a genuine surprise. June US inflation came in significantly softer than expected, triggering a rotation into tech, easing Treasury yields, and giving traders their first clear risk-on signal in weeks. But the reaction was smaller than the data alone would have suggested — and understanding why matters for how the rest of the trading days ahead play out.

The Moves That Mattered

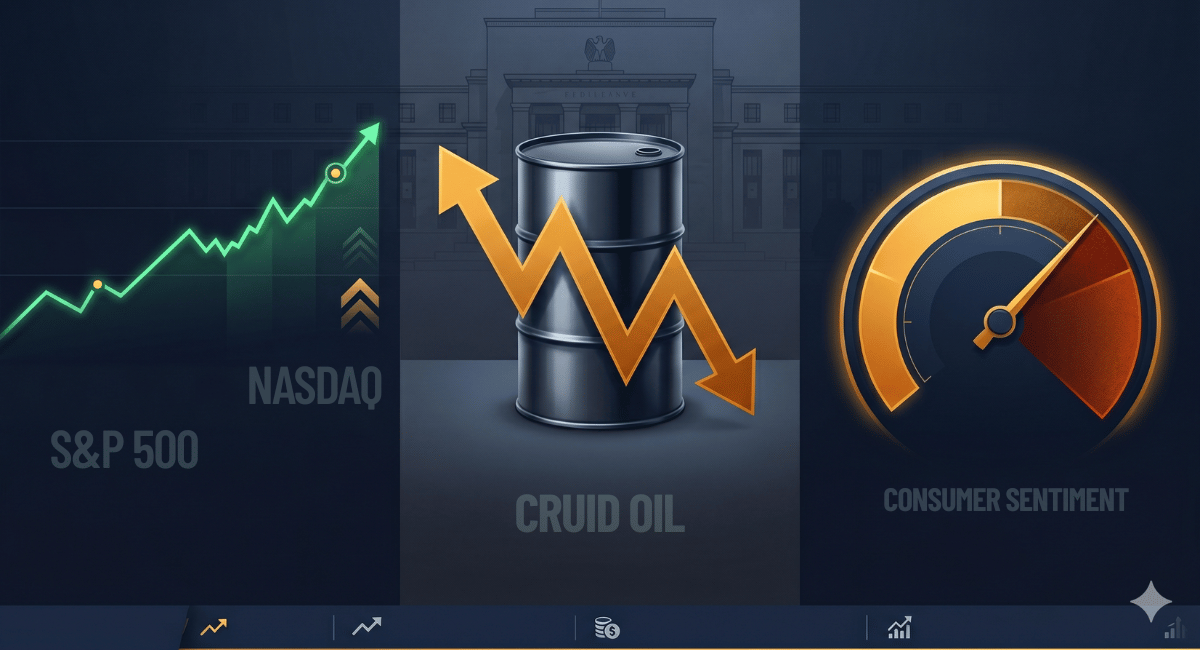

Tech led the rally. The Nasdaq Composite gained 1.1%, the S&P 500 added 0.5%, and the Russell 2000 rose 0.4%. The Dow was an outlier, closing 65 points lower after IBM crashed 25% on disappointing results — its worst single-day drop on record.

In fixed income, the US 30-year Treasury yield eased back toward 5.0% after trading above that level earlier. Softer inflation reduced the pressure on the long end and gave duration-sensitive sectors, including tech and real estate, room to breathe.

Energy told a different story. Brent crude rose 1% to $84.35, while WTI climbed to $78.70, as fresh US-Iran tensions pushed oil back above $80 a barrel. Gold remained under pressure, caught between softer inflation and firm Fed expectations.

Why the Inflation Print Matters

June headline CPI came in at 3.5% year-on-year, down sharply from 4.2% previously. Monthly headline prices actually fell 0.4% — the first monthly decline in six years and the largest since April 2020. Gasoline prices dropped 9.7% and did most of the heavy lifting.

Core CPI, which strips out food and energy, was flat month-on-month and rose just 2.6% year-on-year — well below Wall Street expectations. That is a genuine cooling signal for the Federal Reserve to weigh.

Why the Reaction Was Smaller Than Expected

Fed rate-hike odds barely moved despite the soft print. The reason: new Fed Chair Kevin Warsh used his House testimony hours later to explicitly push back on any dovish read, calling the improvement "welcome" but stating that "one favourable CPI report does not mean the inflation fight is finished." Markets are still pricing roughly a 70% chance of a rate hike by September.

What Traders Are Watching Next

- Warsh's Senate testimony at 15:00 UK time — his second day before Congress

- June PPI release — the next major inflation read

- Bank earnings continuing — Morgan Stanley, Johnson & Johnson, and ASML report

- Oil above $80 — any further escalation between the US and Iran could reignite energy-driven inflation

- The 30-year yield around 5.0% — a decisive break below could extend the tech-led rally

Track all upcoming releases on our economic calendar.

Bottom Line

The soft CPI print handed traders a temporary reprieve, but it did not change the Fed's direction of travel. Nasdaq strength, cooler yields, and a firmer oil market are all coexisting at the same time — an unusual combination that suggests markets are still working out which signal dominates. Volatility is likely to stay elevated around the Senate testimony and PPI release.

Trade Global Markets with KQ Markets

Access US indices and commodities on KQ Markets, and follow our latest trading signals for detailed market setups.

Open an account with KQ Markets today and trade the markets that matter.

This content is for general informational purposes only and does not constitute investment, financial or trading advice. CFDs and Spread bets are leveraged products and carry a high risk of rapid capital loss. Past performance is not a guarantee of future results.